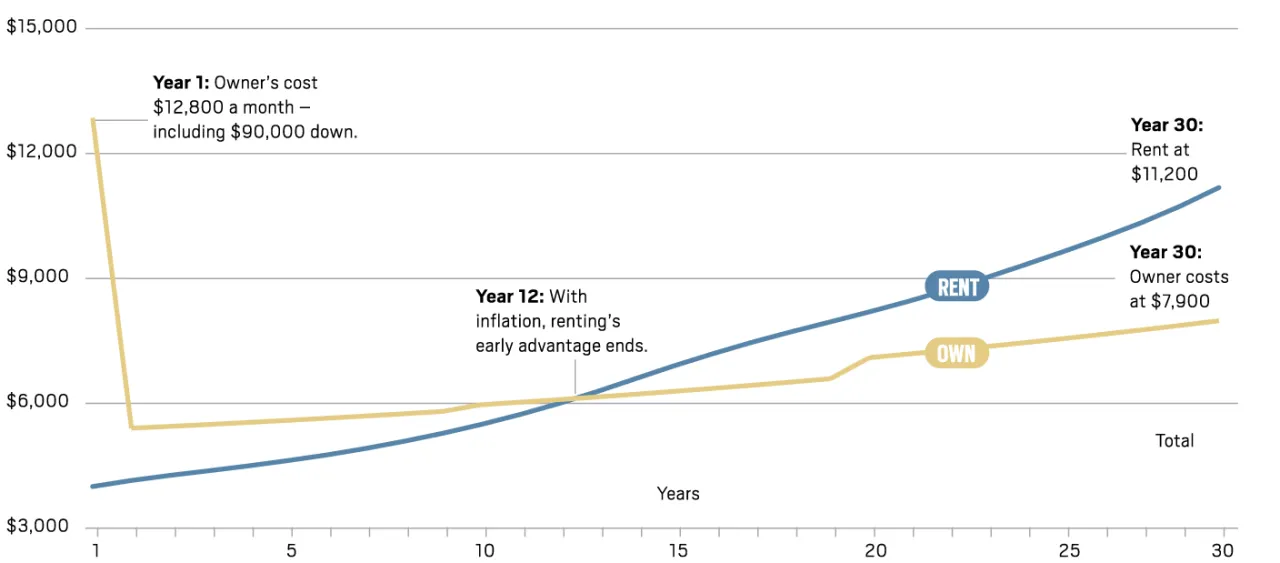

Is It Better to Rent or Own? The debate goes on and on. As a proponent of building wealth through real estate I already know the answer and have blogged about this before. Over the long run it is better to own but over a short period it is better to rent. Somewhere around year 12 of owning, when taking inflation into account, the advantage goes to owners and it continues on from there.

San Diego Union-Tribune (UT) reporters Jeff Goertzen and Jonathan Lansner did a deep dive into the numbers of this in an October 5 article. If you like data you will love this piece and the regular coverage Lansner gives to related topics. It is reason enough to subscribe to the UT! I have borrowed their graphics to illustrate the scenario which estimates California house rent today at $4,000 a month versus buying a $900,000 house with a 10% down mortgage at 6.5% plus property taxes, insurance, association fees, and repairs. The scenario assumes costs grow with historical inflation and the mortgage rate is lowered twice by a half-point through refinancing.

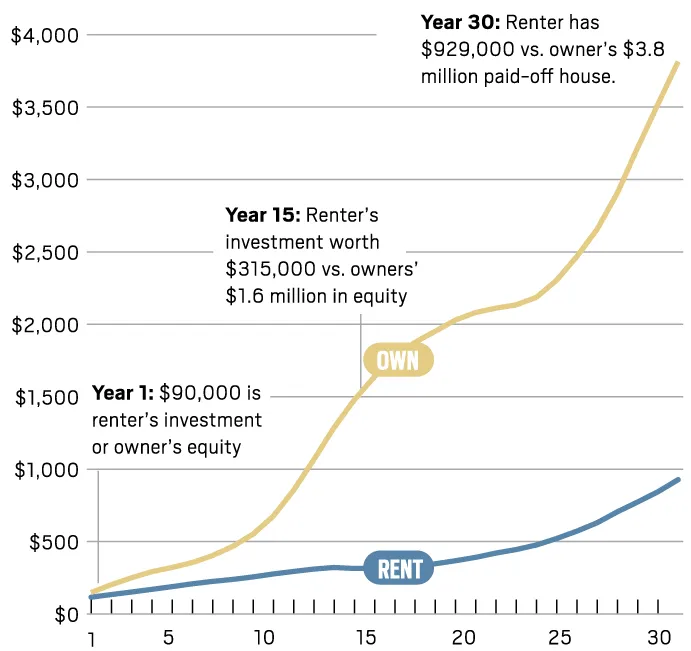

More importantly to note is what appreciation does to the scenario. If you look at this from an investment perspective and treat the home as an asset the value becomes even more apparent. Assuming historical gains of 5% per year, the owners gets a $3.8 million asset after 30 years. The renter, who, in this case, hypothetically invested the $90,000 down payment in the stock market, would accumulate $929,000. Here’s investment value by year, in thousands of dollars.

The bottom line is if you plan to live in the house for 12 years you break even on monthly expenses but even then you will have equity you can capture when you sell which you can take into your next property. Look at the numbers on the graph above. At year 30 would you rather be the renter with $929,000 or the owner with a home worth $3.8 million that is paid off?