High interest rates, hovering around 7 percent right now, are impacting younger buyers who haven't had time to move up the ladder to higher paying jobs. As a result, the median age of a first-time buyer is 36 years old, the oldest it has been since the National Association of Realtors started tracking this data in 1981 when the median-aged buyer was 29 years old.

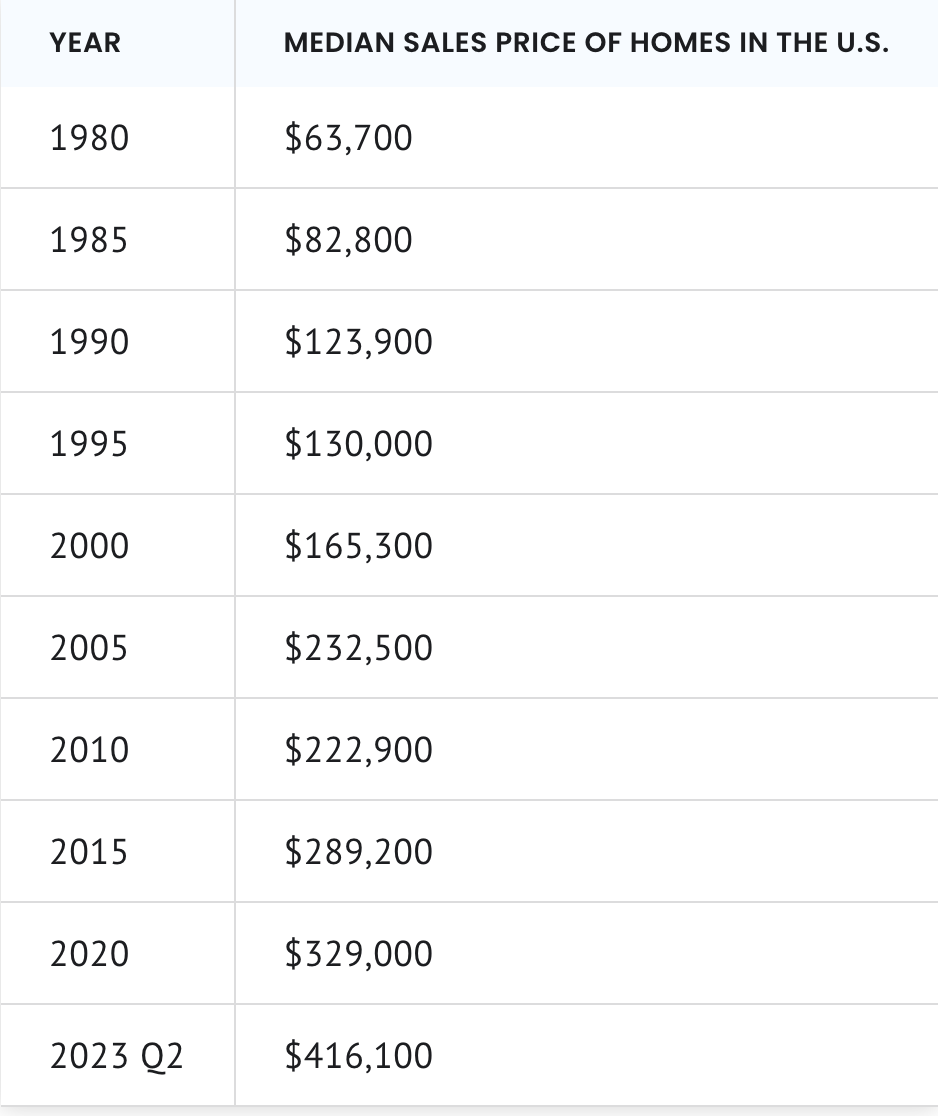

Since the Great Recession, 30-year-fixed mortgages have generally averaged well below 5 percent — substantially cheaper than the six to eight percent range seen in the two decades before, and well below their peak of over 18 percent in 1981. Combine that rate with a national median sales price of more than $416,000 in the second quarter of 2023 and it is a tough market. This number is much higher in San Diego where the median sale price over the last 30 days is $851,000. You can see why people are moving out of state!

According to a July 31 Motley Fool article this is how national median prices have changed:

The answer is more housing but how does that happen? Our government leaders are looking at this issue but it certainly isn't an easy one to solve. The National Association of Realtors is advocating for three things:

1) Increasing the amount of capital gains a homeowner can exclude on the sale of a principal residence and annually adjusting it for inflation. This would incentivize more owners to sell.

2) Offering tax credits to attract private investment for rehabilitating owner-occupied homes in areas where it is often more expensive to rehabilitate than appraisal values will support.

3) Creating tax incentives for conversion of unused commercial buildings to residential and mixed-use properties. We see this happening in California already but tax incentives would really help.

All of these make sense to me and would certainly help bring more inventory to our property-starved market.